Year-end closing is a very important and complex process that results in the preparation of accurate financial statements. Regardless of the country you are in, the result is the same — ASSETS must equal LIABILITIES. And although it may seem simple, in practice it is much more complicated. This is because a number of adjustments and clarifications must be made to correctly determine the value of assets and liabilities. And, of course, each country has its own differences in achieving this coveted goal. Let’s consider some differences between Poland and Belarus.

But first of all, we would like to draw attention to a document called accounting policy, which is the most important document of accounting law and determines the essence of accounting and the preparation of financial statements. Without it, it is impossible to correctly prepare financial statements. However, we often encounter situations in Poland where colleagues say that accounting policy is not mandatory. All the necessary information about the accounting policy can be found in additional information. But how can one reflect transactions in accounting for a whole year if there is no accounting policy?

Important! In Belarus, accounting policy, taking into account changes to the tax code that come into force from 01.01.2024, must be submitted to the tax authority in case of any changes — no later than thirty calendar days from the date of their approval by the organization’s management or other authorized person. A newly created organization in the current year must submit its accounting policy to the tax authority no later than thirty calendar days from the date of state registration of the organization.

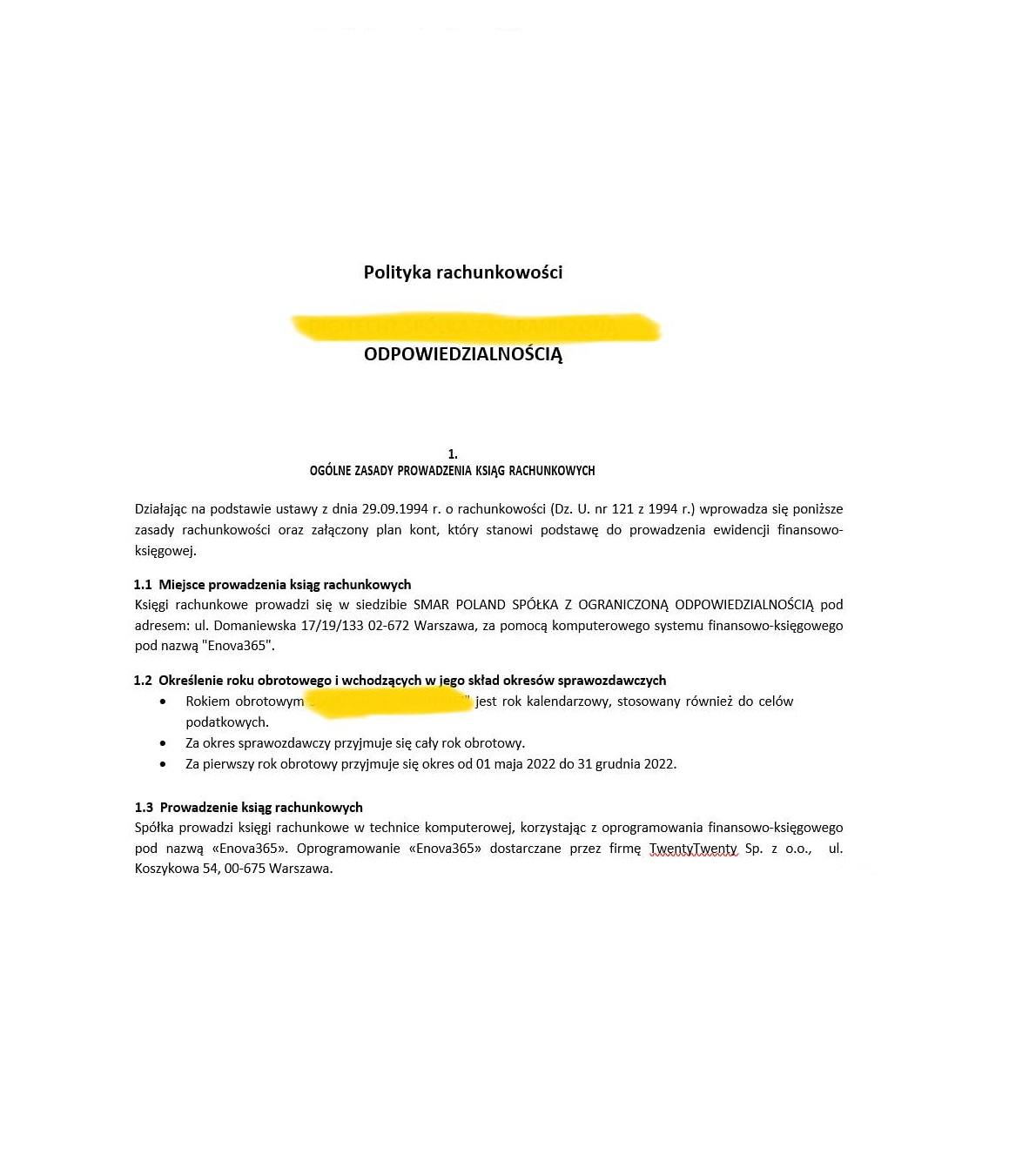

Figure 1 — Example of accounting policy of SMAR POLAND

Difference 1. Determining the need to submit financial statements

In Poland, new companies registered in the current year can choose the financial reporting year not from the moment of registration, but starting from the following year. This avoids the need to prepare reports for an incomplete year and the associated additional expenses.

In Belarus, there is no such right, and financial statements must be submitted for the previous year, even if the company was registered on December 31 (except in cases of accounting in the income and expense book under the simplified tax system).

DIFFERENCE 2. Determination of Annual Reporting Form

Small companies and micro-organizations in Poland have a simplified reporting form, which makes year-end closing easier and allows for the use of a range of simplifications (such as, for example, abandoning the prudence principle in valuation and others).

It is also important to consider the differences in reporting forms for different types of companies, such as banks, insurance organizations, and others.

Which companies are considered micro-organizations?

In Poland, companies that meet the following criteria are considered micro-organizations:

- Balance sheet assets at the end of the financial year amounting to 1,500,000 PLN;

- Net sales revenue for the financial year of 3,000,000 PLN;

- Average annual full-time workforce of 10 people.

For comparison, in Belarus, micro-organizations are registered commercial organizations with an average annual workforce of up to 15 people.

Which companies are considered small organizations?

In Poland, companies that meet the following criteria are considered small organizations:

- Balance sheet assets at the end of the financial year of 25,500,000 PLN;

- Net sales revenue for the financial year of 51,000,000 PLN;

- Average annual full-time workforce of 50 people.

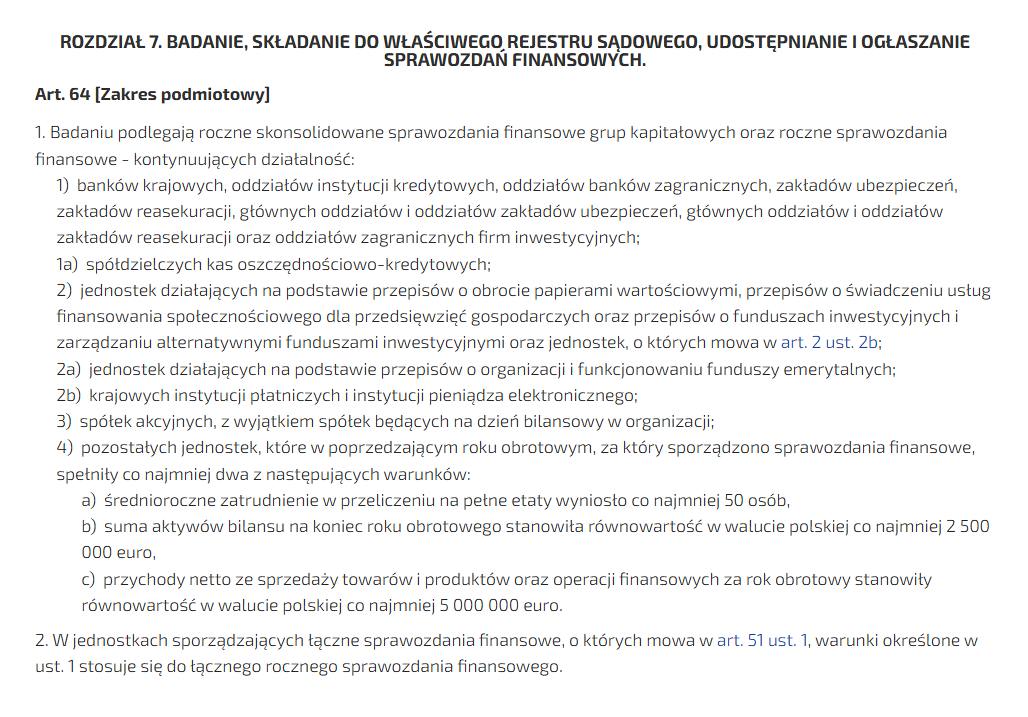

Figure 2 — Article 64 of the Accounting Act (USTAWA O RACHUNKOWOŚCI)

For comparison, in Belarus, small organizations are registered commercial organizations with an average annual workforce of 16 to 100 people.

In Belarus, there is no right to choose the form of accounting reporting (there are differences for banks, insurance companies, and budget organizations), and there is no possibility to choose the annual reporting form based on the size of the company.

DISTINCTION 3. Requirements for mandatory auditing

In Poland, the financial statements of organizations specified in Article 64 of the Accounting Act (Ustawa o rachunkowości) are subject to audit.

These companies can be divided into those that:

- by their nature, will always be subject to mandatory auditing.

For example, the consolidated financial statements of the following entities that continue their activities are always subject to mandatory auditing: national banks, branches of credit institutions, branches of foreign banks, insurance organizations, joint-stock companies (with some exceptions), and others.

- and those that are subject to mandatory auditing after meeting certain conditions. Organizations that, in the previous financial year for which the financial statements were prepared, met at least two of the following conditions:

a) average annual employment on full-time basis was at least 50 people,

b) the balance sheet asset value at the end of the financial year was equivalent to at least 2,500,000 euros in Polish currency,

c) net revenue from the sale of goods, products, and financial operations for the financial year amounted to at least 5,000,000 euros in Polish currency.

In Belarus, there are also organizations that undergo mandatory auditing regardless of the size of the company (part 3 of Article 22 of the Law «On Auditing Activities»): joint-stock companies required by legislation to disclose information about the joint-stock company in accordance with securities legislation; The National Bank; banks, banking groups, banking holdings; exchanges; insurance organizations, insurance brokers, and others. The list is very similar to the Polish one.

We would like to focus on residents of the High-Tech Park, for whom auditing of their financial statements is mandatory. Since there is a deadline for submitting audited reports to the High-Tech Park Administration (by July 1 of the current year for the previous year), it is important to find an auditing company in advance and plan the timeline for conducting the audit and issuing the reports.

And also other legal entities whose revenue from the sale of goods (performance of works, provision of services) for the previous reporting year exceeds 500,000 basic units (as of December 31 of the previous reporting year), i.e. 18,500,000 rubles, which is approximately equivalent to 5,138,000 euros

DISTINCTION 4. Inventory Deadlines

Annual inventory is a complex process that requires careful preparation and is conducted to compare the actual presence of assets and liabilities with the accounting data.

In Belarus, the procedure for conducting inventory of assets and liabilities of organizations, documenting the results of the inventory and reflecting them in accounting is established by Instruction No. 180. Inventory of assets and liabilities must be conducted before preparing the annual financial statements according to the following deadlines (paragraph 3, subparagraph 2, Article 13 of Law No. 57-Z, paragraph 7 of Instruction No. 180):

- fixed assets, intangible assets, unfinished construction, raw materials, materials, finished products, goods for sale (including goods in warehouses, goods in retail trade, packaging for goods and empties, purchased products, agricultural products) — no earlier than November 1st;

- unfinished production and semi-finished products — no earlier than November 1st;

- animals for breeding and fattening (including young animals) — no earlier than November 1st;

- cash — no earlier than December 1st;

- liabilities and other assets — no earlier than December 1st.

In Poland, it is important to see what is specified in each company’s accounting policy regarding the conduct of inventory and to formalize the results of the inventory.

For example, every 4 years (due to the fact that the property is located on protected territory), it is possible to carry out an inventory of fixed assets, machinery, and equipment that are part of fixed assets in construction.

However, on the balance sheet date of each reporting year, the following assets and liabilities are subject to inventory:

- cash assets

- bank loans

- securities

- materials, goods that are to be expensed on the day of purchase,

- assets and liabilities whose condition is determined by verification (Inwentaryzacja w drodze weryfikacji concerns those components of assets and liabilities that cannot be inventoried through a physical count or through reconciliation and confirmation of balances for various reasons.

For example, buildings and structures under construction (excluding machinery and equipment included therein) are verified through this method.

DISTINCTION 5

Criteria for related party transactions

In both Poland and RB, it is important to have information about related parties in order to control operations between them for transfer pricing purposes. It is also necessary to disclose this information in additional information and notes to the financial statements.

It is IMPORTANT to remember the transaction limits for price control.

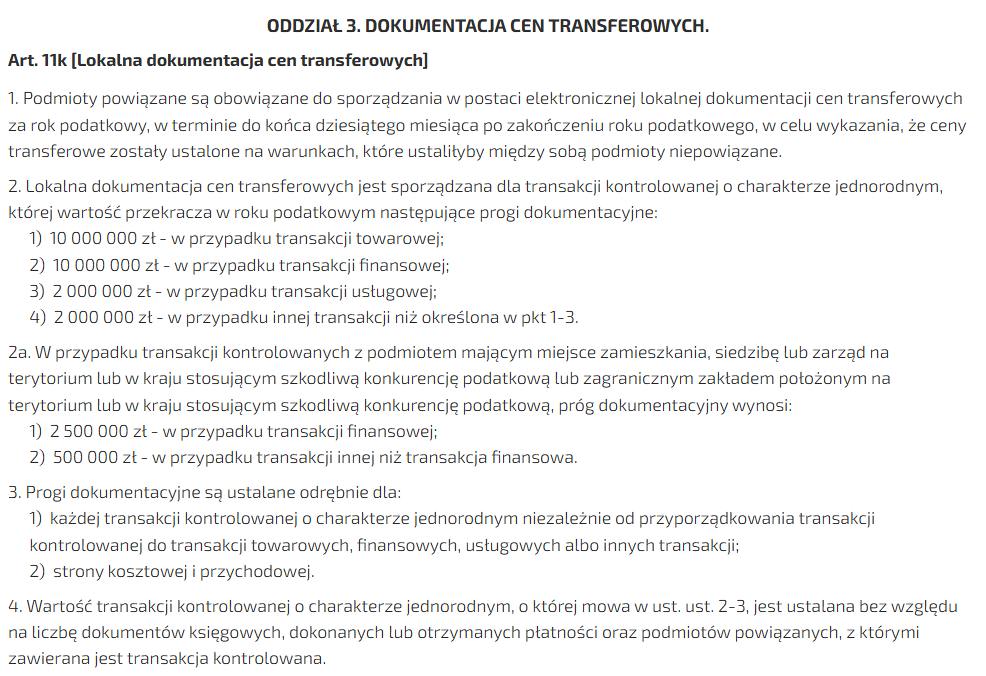

In Poland, mandatory threshold values for preparing transfer pricing documentation are set out in Article 11k (2) of the PDOPrU. According to this provision, local transfer pricing documentation is prepared for a controlled transaction of a homogeneous nature, the value of which exceeds the following threshold values for documentation in the tax year:

- 10,000,000 PLN for a goods or financial transaction,

- 2,000,000 PLN for a service transaction,

- 2,000,000 PLN for any other transaction not mentioned above.

Figure 3 — Art. 11k (USTAWA O PODATKU DOCHODOWYM OD OSÓB PRAWNYCH)

In the Republic of Belarus, for example, a foreign trade deal with a related party is subject to control if it exceeds 400,000 Belarusian rubles (excluding value-added tax and excise tax) for an organization not included in the list of major taxpayers; and if it exceeds 2,000,000 Belarusian rubles (excluding value-added tax and excise tax) for an organization included in the list of major taxpayers, except for transactions specified in subparagraph 2.2 of paragraph 2 of Article 88 of the Tax Code of the Republic of Belarus.

And for transactions concerning the sale or acquisition of goods (works, services), property rights, carried out with a related legal entity — a tax resident of the Republic of Belarus that does not calculate and pay corporate income tax (exempt from corporate income tax) in the calendar year in which the transaction is made — it is subject to control if it exceeds 400,000 Belarusian rubles (excluding value-added tax and excise tax) for an organization not included in the list of major taxpayers; and 2,000,000 Belarusian rubles (excluding value-added tax and excise tax) for an organization included in the list of major taxpayers.

DIFFERENCE 6. Deadlines for preparing, approving, and submitting reports

In Poland, financial statements must be approved by June 30 and filed by July 15.

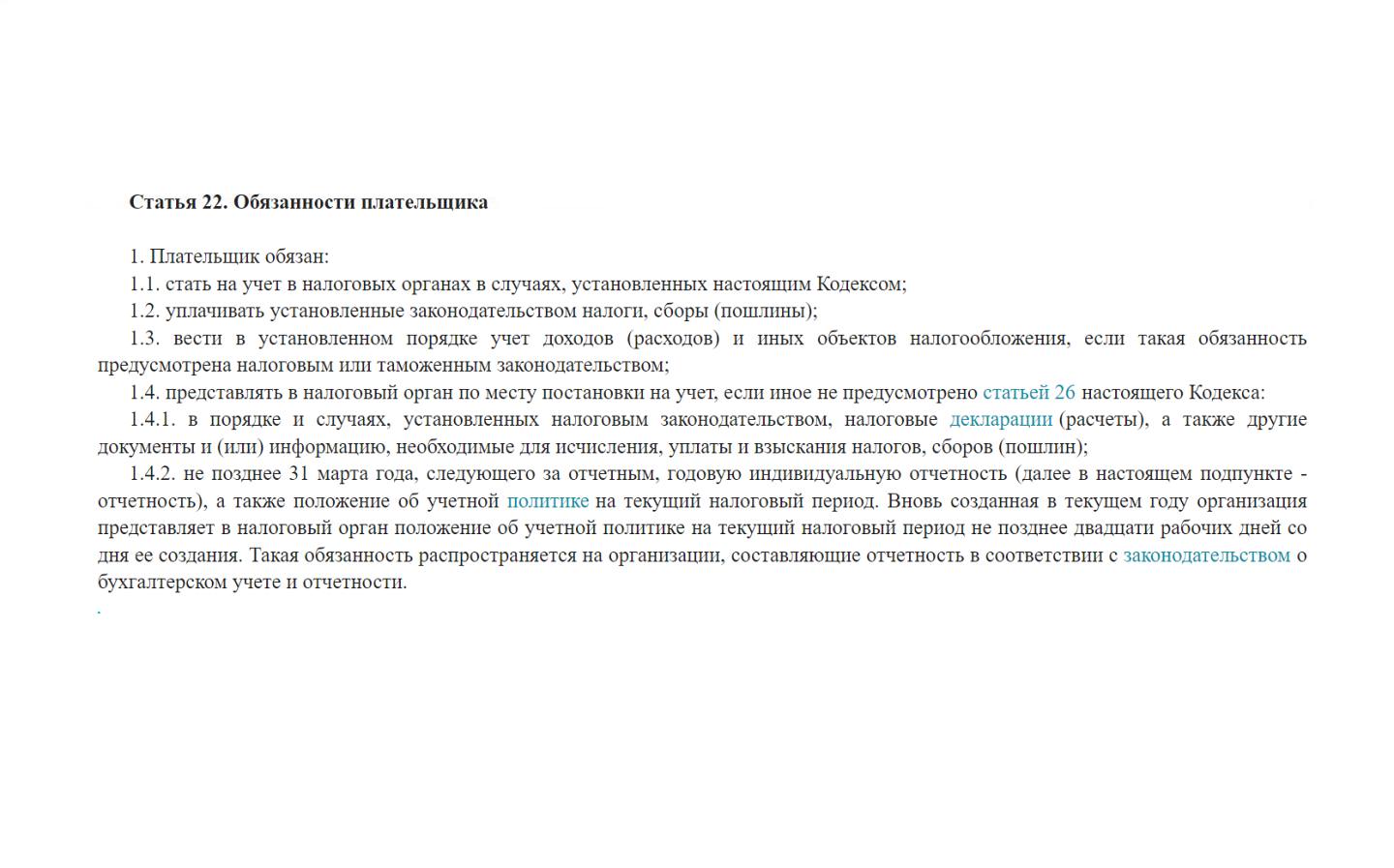

In 2023, organizations in the Republic of Belarus that prepare financial statements in accordance with the accounting and reporting legislation are required to submit their annual individual reports in electronic format to the tax authority at their place of registration no later than March 31 of the year following the reporting period, as well as the accounting policy for the current tax period (part 1, subparagraphs 3 of paragraph 1.4.2 of article 22 of the Tax Code).

Figure 4 — part 1, subparagraph 3 of paragraph 1.4.2 of article 22 of the Tax Code of the Republic of Belarus.

Failure to submit financial statements to the tax authority within the specified deadline in the Republic of Belarus may result in administrative liability and a fine of up to 20 base amounts (part 1 of article 14.6 of the Administrative Offenses Code). Violation of the established procedure for conducting accounting and reporting by officials of the organization entails administrative liability in the form of a warning or a fine of up to 20 base amounts (part 1 of article 12.32 of the Administrative Offenses Code).

In Poland, there is a serious penalty for failure to submit an annual report, ranging from a fine to up to two years of imprisonment.

These are just a few differences in the year-end closing and preparation of financial statements in Poland and the Republic of Belarus. The year-end closing process is quite complex and involves many aspects (such as the thin capitalization rule, provision for doubtful debts, and much more).

If you have any questions and need consultation, our team at SMAR POLAND will be happy to assist you.